Key Takeaways

- OBBBA Opportunity Zones.

- Number of itemizers estimated under OBBBA.

- Changes to gambling deductions.

- International retaliatory taxes.

- "Crypto Week" in Washington.

- National Lottery Day!

One Big Beautiful Bill Act

GOP Reshapes Opportunity Zones to Target Trump Country - Richard Rubin and Ruth Simon, Wall Street Journal:

For Opportunity Zones 2.0, Republicans reshaped the program to aid rural America, testing whether bigger tax breaks can bring investment to areas largely left behind by a program for left-behind areas.

...

The extension and changes should reduce federal revenue by $41 billion through 2034, according to the Joint Committee on Taxation. The biggest visible shift is the rural emphasis. Starting in 2027, after governors designate new zones, capital gains placed into rural investments and held for five years can receive a 30% tax discount, triple the benefit elsewhere. Rural projects will qualify for incentives with lower thresholds for investments in existing structures.

T25-0243 – Impact of the 2025 Reconciliation Act on the Number of Itemizers, 2025-35 Calendar Years - Tax Policy Center:

Between 2026 and 2029, that share of itemizers will grow to about 14 percent in 2029 (or roughly 27 million itemizers). After 2029, the share of itemizers will drop to around 11 percent, primarily because the increase in the SALT limit will expire and return to $10,000 (not indexed for inflation).

Republican Tax Bill Is a Losing Deal for Gamblers - Alan Rappeport, New York Times:

...

Many Republicans have said they were not even aware how the tax change got into the bill, and this week Democrats from Nevada tried without success to belatedly reverse it.

“If you’re asking me how it got in there, no I don’t know,” Senator Charles E. Grassley, an Iowa Republican who sits on the Finance Committee, told reporters last week.

International

Tax News & Views International Weekly: Retaliatory Tools - Alex Parker, Eide Bailly:

...

But while that largely removed the possibility of new retaliatory taxes over the global minimum tax, also known as Pillar Two, it’s not entirely gone. So far, none of the parties have released any further details about the “joint understanding,” which for now seems more like a high-level handshake agreement than a formal truce. There are still many questions about how this understanding could work in practice.

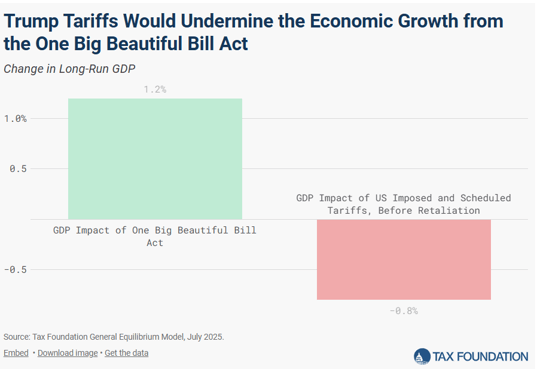

Trump Tariffs Threaten to Offset Much of the “Big Beautiful Bill” Tax Cuts - Erica York and Alex Durante, Tax Policy Blog:

Related: Eide Bailly International Tax Services.

This week on Capitol Hill - Digital Assets

House Taxwriters Shift Focus to Digital Asset Tax Treatment - Cady Stanton, Tax Notes ($):

Ohio Republican plans to lead comprehensive tax overhaul for crypto - Benjamin Guggenheim, Politico:

The bill would clarify the taxation of staking, which involves crypto users pledging their digital assets to help validate transactions, and could modernize “wash sale rules” that prevent investors from taking short-term losses on crypto to wipe out their tax liabilities. Miller also said he wants to improve the treatment of digital assets in qualified retirement plans, loans and charitable contributions.

IRS addresses withholding on uncashed retirement plan payments

IRS Addresses Uncashed Retirement Plan Distributions - Tax Analysts, Tax Notes ($):

...

The IRS ruled that no adjustment or refund is available under sections 6413 and 6414 for the amounts withheld and remitted regarding the first check. The IRS also determined that if the amount of the individual’s accrued benefit under the plan at the time of issuance of the second check is less than or equal to the amount of the first check, no federal income tax withholding obligations apply regarding the second check. Moreover, if the amount of the individual’s accrued benefit at the time of issuance of the second check is greater than the amount of the first check, the excess amount is subject to withholding in accordance with section 3405.

Blogs and Bits

Tax pros should watch out for phishing emails and other attacks, Security Summit warns - IRS:

Deciding whether to convert your hobby to a business - Kay Bell, Don't Mess with Taxes:

- Do you intend to make a profit?

- If the activity makes a profit, how much is it?

- Can you expect to make a future profit from the appreciation of the assets used in the activity?

- Do you depend on income from the activity for your livelihood?

- Are any losses due to circumstances beyond your control or are the losses normal for the startup phase of your type of business?

- Do you adjust operations to improve profitability?

- Do you carry out the activity like a business, keeping complete and accurate books and records?

- Do you and your advisors have the knowledge needed to carry out the activity as a successful business?

In the Courts

A Critical Review of Veribest Vesta, LLC v. Commissioner of Internal Revenue: Implications for Conservation Easement Valuations - Ed Zollars, Current Federal Tax Developments:

Tax Trouble

What day is it?

It's National Lottery Day!

Make a habit of sustained success.